The “Sleep-Well-at-Night” Strategy

How Government-Backed Rent Can Support Steady Cash Flow—and Why the Social Impact Is the Point, Not the Pitch

If you’re like most everyday investors, you’re not hunting for the next rocketship. You’re hunting for something far more useful: a strategy you can actually understand—one where the cash flow makes sense, the demand is real, and the outcome doesn’t depend on perfect timing or a lucky exit. You want something that feels steady. Something that fits the part of your portfolio you don’t want to babysit.

That’s the lens behind the RentSURETY Housing Stability Fund. At its core, the fund is designed to turn a messy, inefficient part of the housing market into something more predictable—not by “hoping” the world behaves, but by changing the payment experience for landlords in a way that makes them meaningfully more willing to accept voucher holders. And as a result, more families—especially veterans, disabled individuals, and other voucher-supported households—can actually secure housing rather than getting stuck in limbo.

To understand why this matters, it helps to start with an uncomfortable truth: in the Housing Choice Voucher (often called “Section 8”) world, the biggest barrier to housing access usually isn’t whether rent will be paid. It’s whether the process will be smooth. A lot of people assume Section 8 is risky. But voucher holders often struggle to rent not because the rent is “bad” or unreliable, but because landlords anticipate friction—paperwork, inspections, timelines, uncertainty around when payments start, and the general fear that “this will be a hassle.” That fear becomes the decision. And when enough landlords make that decision, you get a market that doesn’t clear—even when both renters and rentals are plentiful.

That’s not really “tenant risk.” That’s process risk. And process risk creates a weird situation that’s easy to miss if you only look at the market through stereotypes: there’s an underutilized, high-quality rent payment stream supported by government reimbursement mechanics, but it stays underused because landlords don’t want the uncertainty and administrative drag. In other words, the challenge isn’t the existence of payment support—it’s the experience of receiving it consistently and on time in a way that matches how landlords run their businesses and pay their own bills.

For investors focused on stability, this is exactly the kind of setup that can create a durable opportunity. You’re looking for situations where demand is strong and consistent, cash flow is tied to something real and persistent, and the opportunity exists because the market is inefficient. That’s what’s happening here. There are lots of voucher holders trying to find housing, and there are lots of rentals that need tenants—but the match breaks down because landlords hesitate. When you can fix the reason they hesitate, you can move the whole system toward stability: fewer vacancies, smoother lease-ups, and a more predictable rent collection experience.

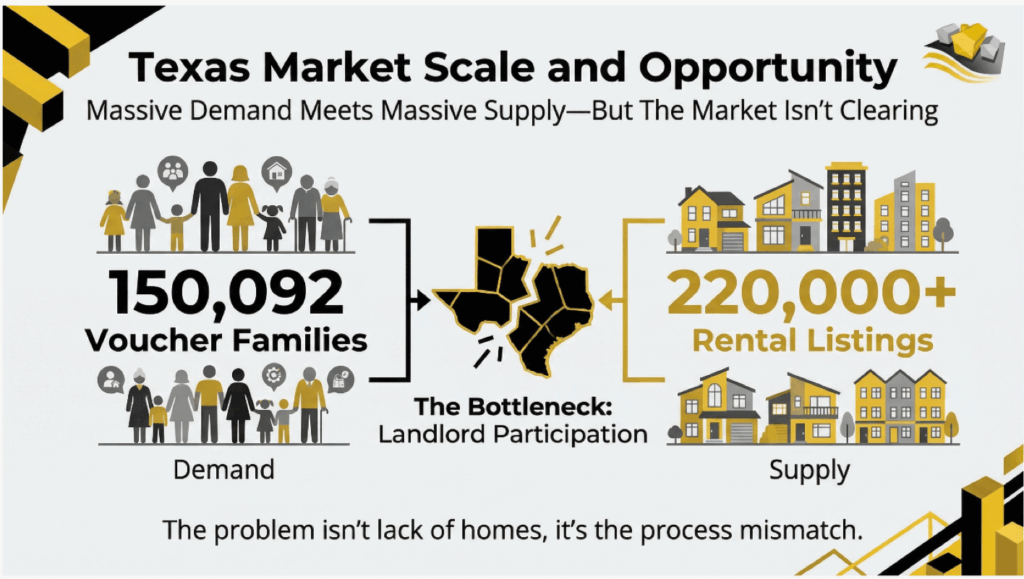

Texas is a great example of the scale we’re talking about. It isn’t a small market; it’s enormous. According to NAHRO’s September 2025 state data flyer, Texas has 150,092 families with a Housing Choice Voucher. On the supply side, the rental inventory is massive too. In mid-January 2026, Realtor.com showed 109,964 apartments and homes for rent in Texas, and Zillow showed 220,328 rental listings in Texas. Either way, we’re clearly talking about well over 50,000 rentals available at once, which means there’s plenty of inventory to fill. So why aren’t voucher holders getting housed faster? Because the market isn’t clearing smoothly. The bottleneck isn’t “no homes exist.” The bottleneck is the mismatch between voucher demand and landlord participation.

Now here’s where the social impact becomes very real—because behind the phrase “voucher holder” are actual people with actual constraints. A large share of voucher households include individuals who need stability the most: families with children, seniors, veterans, and people living with disabilities. For a disabled individual—especially someone on a fixed income—housing instability doesn’t just mean inconvenience. It can mean missed medical appointments, lost access to caregivers, disrupted benefits, and the kind of stress that makes everything else in life harder. Housing is not just shelter; it’s the foundation that allows people to manage health, maintain routines, and participate in daily life.

And yet, the system can put those individuals through an exhausting obstacle course. Imagine being voucher-approved, knowing you have support, and still being turned away repeatedly because landlords fear the process. That’s demoralizing in any circumstance. But for a disabled person who can’t “just keep touring units,” or for a veteran navigating transitions, or for a parent working two jobs—it becomes a structural barrier. That’s why we say this isn’t merely a housing problem. It’s a stability problem. And stability—both financial and human—depends heavily on one thing: consistent monthly payments that people can rely on.

Landlords want predictable income. Period. They have mortgages, taxes, maintenance costs, insurance, payroll, and their own cash-flow planning. When a landlord hears “voucher,” many don’t think “guaranteed rent.” They think: “This will take longer.” “Payments might be delayed at the beginning.” “It might be more work than it’s worth.” So even when rent is supported through established program channels administered by public housing authorities, many landlords still pass. That’s the core problem the fund is designed to solve: landlord acceptance is constrained by friction—not credit.

Here’s the RentSURETY structure in plain English. First, a landlord signs a new lease with a voucher holder. Then, the fund advances the landlord 11 months of rent upfront at lease signing. After that, the fund receives consistent monthly rent payments through the government reimbursement-backed voucher channel. Finally, the fund retains 1 month of rent as a fee for providing the upfront capital and running the process. When you put that in the landlord’s shoes, you can see why it changes behavior almost instantly: when a landlord gets 11 months of rent upfront, a huge amount of worry disappears immediately. They stop thinking, “How long will this take?” “Will this be complicated?” “Will payments start late?” And they start thinking, “I just got paid,” “This unit is filled,” and “My cash flow is stabilized.”

That emphasis on consistency of rental payments is not a small detail; it’s the entire strategy. Consistency is what landlords optimize for, and it’s what stability investors optimize for too. When payments arrive predictably, you reduce stress in the system. You reduce turnover. You reduce the number of “almost move-ins” that fail because the process dragged out too long. You reduce the incentives for landlords to avoid vouchers. And most importantly, you reduce the number of families who fall through the cracks simply because nobody could coordinate a clean lease start.

This is where the social impact becomes more than a talking point. When a market clears more efficiently, real lives stabilize. Consider a disabled individual who needs an accessible unit and can’t easily move again if the lease falls apart. Or a veteran who needs a stable address to maintain employment, benefits, and healthcare continuity. Or a family with children who need consistency in schooling. When landlord participation increases and leasing becomes smoother, these households don’t just “get housed.” They get the ability to plan. They get to exhale. They get stability that compounds over time, the same way predictable financial cash flow compounds value in a portfolio.

And there’s another layer: the strategy doesn’t ask landlords to “be nicer” or “take one for the team.” It doesn’t rely on changing hearts and minds through moral arguments. It changes the outcome by changing the incentives and the payment experience. That’s why it can scale. Stigma often exists because people don’t trust what they can’t predict. When the payment experience becomes predictable—when landlords see a clean, consistent result—stigma loses power. It becomes hard to hold onto bias when the transaction performs.

A single clever deal isn’t an investment strategy. A real strategy needs a repeatable process—something you can do again and again in a way that doesn’t depend on luck, doesn’t require perfect market timing, and can scale responsibly. This model is designed to be repeatable because it follows a consistent loop: identify available rental inventory; work with landlords who value certainty; help convert voucher demand into signed leases; execute the advance; service and monitor payments; track outcomes; and keep improving the process. That repeatability matters because it’s the difference between a story and a system. Investors don’t allocate to stories. They allocate to systems.

This is also why the fund’s social impact is not a separate charity layer bolted on the side. It’s built into the mechanics. When landlords become comfortable accepting voucher holders, more families get housed. That includes veterans and disabled individuals who rely on stable housing to rebuild and maintain stability. And when more families get housed, fewer households get stuck in limbo, fewer units sit vacant, and the housing market becomes more efficient for everyone. That’s impact you can measure, because it comes from real transactions—not slogans.

It’s worth pausing here to be clear about one important point: none of this should be interpreted as “guaranteed returns” or “risk-free.” All investing involves risk, including the loss of principal. Any model that touches real-world payments involves timing, operations, and execution. The difference is that this strategy is designed specifically to reduce one of the biggest barriers in the voucher market—process friction—by engineering landlord certainty upfront and building a repeatable operational system around consistent monthly payment mechanics.

When you step back, you can see why this fits stability-minded investors. The thesis is not “housing prices will go up.” The thesis is: housing demand is persistent, voucher demand is real and funded, and the market is inefficient because the process is painful. If you can remove that pain—if you can make rental payments consistent and the landlord experience predictable—you can unlock participation, improve outcomes, and create a system that behaves more steadily.

Want the details? Request the Investor Overview to see the full model, how the process works, and the risk considerations.