Why Rent Is One of the Most Reliable Cash Flows in Private Credit

For decades, income-focused investors have relied on a familiar toolkit: public bonds, dividend-paying equities, REITs, and yield-oriented mutual funds. While each has its place, these instruments increasingly share a common vulnerability—they are exposed to market volatility, interest rate risk, and investor sentiment rather than to predictable, contractual cash flows.

At Ten Bridge Capital, we believe many investors underestimate one of the most resilient and intuitive income sources in the economy: residential rent.

The RentSURETY platform was built on a simple but powerful observation—one that landlords understand instinctively, yet capital markets often overlook. Rent behaves differently than most forms of consumer or corporate credit, particularly during periods of economic stress. This distinction makes rent-backed obligations uniquely suited for short-duration, income-oriented private credit strategies.

Rent Is Not Discretionary

Unlike most household expenses, rent is not optional. It is not a lifestyle upgrade, a convenience, or a luxury. Housing sits at the top of the payment hierarchy for households across income levels.

Empirical behavior during economic downturns consistently shows that when budgets tighten, tenants adjust elsewhere first. Dining, travel, entertainment, retail purchases, and even certain debt obligations may be delayed or reduced. Rent, however, remains a priority because the consequences of non-payment are immediate and existential.

From a credit perspective, this creates a meaningful distinction. Rent payments are:

•Behaviorally prioritized

•Contractually obligated

•Recurrent and predictable

•Directly tied to shelter

This behavioral reality is foundational to how rent-backed credit differs from unsecured consumer debt or speculative financial instruments.

Why Rent Performs Differently Than Other Credit

Traditional consumer credit products—credit cards, personal loans, auto loans—are often unsecured, long-dated, and sensitive to consumer sentiment. Corporate debt, meanwhile, is exposed to earnings volatility, refinancing risk, and capital market conditions.

Rent-backed obligations operate under a different framework.

Key characteristics include:

•Monthly reset cycles that limit duration risk

•Short contractual timeframes compared to long-term bonds

•Direct linkage to a physical housing unit

•Clear enforcement mechanisms embedded in lease agreements

•Local market accountability, not abstract corporate performance

These structural features allow rent-backed credit to function as a form of short-duration, self-amortizing exposure rather than a long-term bet on future conditions.

Landlords Already Think Like Credit Investors

One of the reasons rent-backed private credit resonates with landlords is that they already evaluate tenants through a credit lens—often more conservatively than institutional lenders.

Before approving a tenant, landlords routinely assess:

•Prior rental payment history

•Income sufficiency and stability

•Lease terms and duration

•Behavioral indicators and references

•Local market demand

This process mirrors how institutional credit managers evaluate counterparties: focus on cash flow reliability, downside risk, and the probability of repayment rather than theoretical upside.

The RentSURETY platform institutionalizes this logic—applying consistent underwriting standards, verification processes, and servicing protocols across thousands of rent obligations rather than individual units.

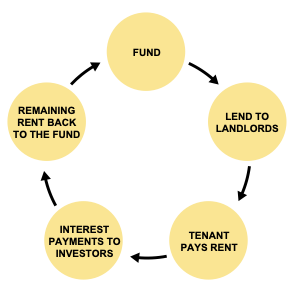

From Individual Leases to Diversified Cash Flow

On their own, individual rental payments are fragmented and operationally intensive. What private credit structures allow is aggregation, diversification, and professional management.

Across the RentSURETY family of funds, capital is deployed into short-duration financing arrangements secured by pledged tenant rental payments and verified lease performance. Depending on the fund and structure, these arrangements may include:

•Rent advances to qualified landlords

•Pay-as-due rent programs that smooth monthly collections

•Limited-duration rent protection during defined default or eviction periods

As rent payments are collected, they are serviced through structured systems designed to prioritize predictability, transparency, and cash-flow continuity.

For investors, this transforms a familiar asset—rent—into a professionally managed income stream.

Defensive Characteristics in Volatile Markets

Rent-backed private credit is not designed to outperform during speculative market booms. Instead, it is structured to perform consistently across cycles.

Its defensive characteristics include:

•Low correlation to equity markets

•Limited exposure to interest rate duration

•Monthly cash flow reset

•Conservative advance rates

•Loss reserves and structural protections

Because the underlying exposure is short-term and cash-flow driven, the strategy avoids many of the risks that challenge traditional fixed income during periods of rising rates or market dislocation.

Income First, Appreciation Second

A defining feature of rent-backed credit strategies is the emphasis on income over appreciation. Returns are generated from contractual payments, not from asset price movements, refinancing assumptions, or exit multiples.

This distinction matters.

For investors seeking dependable income—particularly retirees, income allocators, and self-directed IRA investors—predictability often outweighs growth. Rent-backed private credit aligns with this objective by prioritizing steady distributions and capital preservation rather than speculative upside.

Professional Structuring Matters

While rent itself is familiar, structuring rent-backed credit responsibly requires discipline. The difference between a durable income strategy and an unstable one lies in:

•Underwriting standards

•Advance limits

•Servicing capabilities

•Reserve policies

•Diversification

•Governance

The RentSURETY platform emphasizes process over promotion. Every structure is designed with downside scenarios in mind first, ensuring that income generation is supported by realistic assumptions rather than optimistic forecasts.

Why This Matters for Investors Today

Many investors are re-evaluating traditional income sources. Public fixed income has become more volatile. Equity dividends fluctuate with earnings. Real estate appreciation is cyclical and sensitive to financing conditions.

Rent-backed private credit offers an alternative rooted in:

•Essential housing demand

•Behavioral payment priority

•Short-duration exposure

•Transparent cash-flow mechanics

For landlords, this strategy feels intuitive. For investors, it provides a way to access income streams tied to an asset class they already trust.

Looking Ahead

Over the coming weeks, we will explore:

•How rent-backed private credit compares to traditional fixed income

•How risk is managed across different RentSURETY strategies

•Why multi-strategy approaches can improve income stability

•How government-supported rent programs add an additional stability layer

Our goal is not to persuade, but to educate—allowing investors to evaluate whether this approach aligns with their income objectives and risk tolerance.

For those interested in learning more about the RentSURETY platform or discussing the structure in greater detail, we welcome the opportunity for a conversation.

Important Disclosure

This communication is for informational purposes only and does not constitute an offer to sell or a solicitation of an offer to buy securities. Any offering will be made only to eligible investors through formal offering documents, including a Private Placement Memorandum. Investing involves risk, including the possible loss of principal.